This article was first published by Tech for Impact on 24 July 2020.

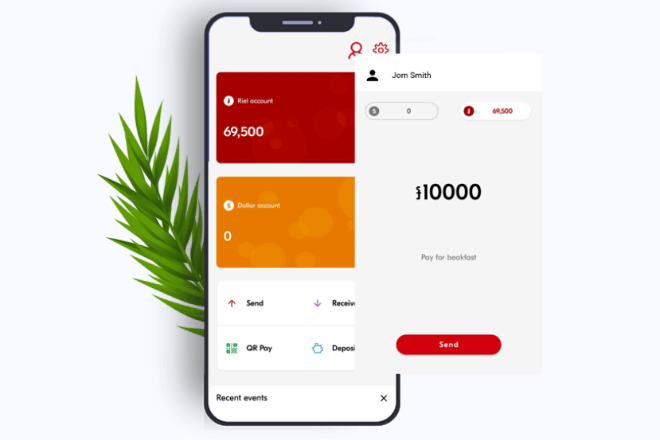

The screen is simple. A red rectangle with your US dollar account and a yellow rectangle with your local currency account. Underneath are four white buttons with the options: send, receive, QR code, and deposit.

So far so… normal.

But what marks out this digital payments system is the fact that it’s all based on one of the most cutting-edge technologies out there, and that it’s been launched in one of ASEAN’s smallest countries—Cambodia.

Launched by the National Bank of Cambodia (NBC) and Japanese tech firm Soramitsu, the Bakong app, originally named Project Bakong, offers users in cities the means to send money back to their families in rural areas. It’s an experience familiar to a quarter of Cambodia’s 15 million population, the 4.1 million who migrate within the country each year. And soon it will be available to Cambodians outside the country, too.

Why use a blockchain backbone in the Project Bakong Wallet?

The long-term strategic goal for the NBC is to reduce the reliance of Cambodians on the US dollar and increase the use of the Cambodian riel. But with the exchange rate at KR4,000 to $1, carrying US dollars means not having to carry around copious amounts of banknotes. A digital cash alternative for the riel is a practical solution, and the blockchain provides it, with an added functionality of being able to bypass commercial banks.

“Due to problems in the past, many Cambodians have an inherent distrust of their banking system,” says Makota Takemiya, CEO of Soramitsu. “Previously in Cambodia, clearing happened twice a day. After a public holiday—when transactions had built up—the system would often crash. By using a blockchain, transaction clearing can happen in real time.”

But even though Bakong competes with local commercial banks, in the long term it’s hoped that it could re-establish trust in the banking system as a whole.

A roadmap for ASEAN?

The real value of the system, however, will be in cross-border transactions. Cambodians based overseas sent home $1.6 billion in 2019, with fees as high as 11.8%. Across Asia, almost $2.46 trillion in digital payments transactions take place every year.

Blockchain can reduce those fees by reducing the need for banks to transport cash to remote areas, and NBC is hoping this solution will be easy to scale throughout the region.

“The technology behind Project Bakong is relatively easy to use in other countries,” says Ales Zivkovic, Soramitsu’s Chief Technology Officer. “The rules we’ve programmed into the Project Bakong wallet that suit Cambodia can be adjusted to suit other countries.”

But what would an international payments system look like? “The most likely international payments system to deal with will be a patchwork of national systems integrated via QR codes and bilateral agreements,” says Zennon Kapron, CEO of KapronAsia, a payments consulting and intelligence service.

According to Takemiya, several other Southeast Asian countries are looking at replicating the Bakong wallet in their countries. But internationally, says Kapron, “the biggest challenge for cross-border payments is organizing cooperation between countries with bilateral agreements. ASEAN has been working on a Southeast Asian payments system for about 10 years already.”

Network dead-zones

“The challenge for app-based payments systems is that they need smartphones, but for many countries, feature phones are still the norm,” says Kapron.

Another obstacle is readiness. Digital banking is still very new in many countries, which means that regulatory infrastructure and education is lagging in places. In Cambodia, citizens can sign up to the app with their ID and a selfie, but electronic know your customer (eKYC) regulations are yet to be written.

Takemiya identifies the knowledge gap as the biggest challenge for Bakong. “It took a little time to explain to the Cambodian people why we were using blockchain, what it was, and how they benefited,” he explains. Once Cambodians understood they were supportive of the pilot.

The next steps for Bakong

The next version of the Bakong wallet will include businesses that accept payments for goods and services through the app, displayed on a map.

Meanwhile, tests of cross-border payments are already under way with Maybank in Malaysia, using QR codes, to demonstrate how the technology can operate as part of an international payments and remittances system.

Although the full potential of blockchain, and products based upon it, has yet to be fully explored, developments like this are pointing towards a radically different financial landscape in ASEAN in the coming years. For now Cambodia looks well positioned to continue leading the initiative.

This article was authored by Sarah Lewis.