Expanding Financial Inclusion for Low-Income Women in the Philippines

Principal Economist, Private Sector Operations Department, Asian Development Bank

Consultant, Asian Development Bank

Associate Economics Officer, Private Sector Operations Department, Asian Development Bank

Pet shop owner Josefina Maranan shares her experience at a briefing for new customers of the Center for Agriculture and Rural Development, Inc. Photo by Al Benavente/ADB.

A $10 million loan from ADB enables a microfinance NGO to reach more borrowers in underserved areas.

This article is adapted from The Transformative Power of Inclusive Business: Case Studies on How Commercially Viable Projects Drive Development published by ADB in December 2024.

In Quezon City, the most populous city in the Philippines, Josefina Maranan and Rowena Sedeño share a common journey of resilience and empowerment as women micro-entrepreneurs. Both are supported by the Center for Agriculture and Rural Development Inc. (CARD, Inc.)—a microfinance nongovernment organization (NGO) dedicated to poverty alleviation and rural development through commercially driven microfinance and community development programs—to pursue their entrepreneurial dreams and achieve their families’ aspirations.

Maranan supplements her family’s income by running a small aquatic pet shop, while Sedeño offers e-loading and payment services.

Micro, small, and medium-sized enterprises (MSMEs) serve as the backbone of the Philippine economy, accounting for 99.6% of all business establishments and 67.0% of the country’s workforce in 2022. However, MSMEs face substantial challenges, primarily because of limited access to capital. Access to funding is often essential for micro-entrepreneurs to take advantage of the opportunities they identify within their local environment.

Local banks tend to perceive MSMEs as high-risk borrowers because they lack credit history and have limited management and financial capabilities. Serving them comes with high administrative costs because of the small amounts MSMEs need or are able to borrow. This risk perception makes it difficult for MSMEs to secure the necessary financing to sustain and grow their businesses.

The COVID-19 pandemic exacerbated these challenges, severely impacting microborrowers, who were among the hardest-hit segments of the economy. Extended lockdowns and ongoing uncertainty forced many microborrowers to close their businesses as revenues plummeted. The pandemic also disrupted household incomes because of job losses and salary cuts. Restrictions on cross-border travel hindered the deployment of migrant labor, aggravating joblessness and reducing remittances.

As COVID-19 created a greater need for borrowing capacity and capital, CARD, Inc. saw an opportunity to collaborate with ADB to expand financial inclusion in the country, driven by a shared vision for empowering people and communities. Its capacity to provide livelihoods to microborrowers, mostly low-income women and farmers, was further enhanced with ADB’s $10 million loan package. The loan enables CARD, Inc. to reach more microborrowers, particularly in remote and underserved areas, providing essential financial resources to those who typically lack access to conventional banking services. By supporting those affected by the economic disruptions of COVID-19, the project helps in the recovery and sustainability of small businesses, thereby stabilizing household incomes and enhancing community resilience.

Accelerating microbusiness operations

Maranan’s journey with CARD, Inc. began in 2010 with a first microloan of ₱3,000 ($53). After the pandemic, it was also CARD, Inc. that brought her business back to life. CARD, Inc. helped Maranan recover from the pandemic when her pet shop temporarily closed down because of COVID-19 restrictions.

“As a plain housewife, I am amazed that a company would trust me to borrow money. It’s empowering,” Maranan shared, adding that she had always dreamed of contributing to her family’s income despite her husband’s steady, albeit low-paying, job as a private school teacher.

Her positive experience led her to encourage her family members to join CARD, Inc. as well. “As a family, our goal was to send our children to school and have food on the table. CARD, Inc. helped us achieve this with their education loans and microloans,” Maranan recalled.

Other financing institutions, she said, had higher interest rates, but CARD, Inc.’s rates appeared to be much lower. Maranan appreciated the straightforward loan application process, which required only a business proposal, site verification by an account officer, and validation by the unit manager.

“My determination to succeed was my only collateral, and it motivates me to make timely payments and build a good credit history,” she said.

Maranan expanded her inventory in 2023 through a ₱20,000 ($350) loan, stocking up on fish, fish food, and other aquatic supplies. This allowed her to meet growing demand as businesses recovered from the pandemic. The loan was payable at ₱515 ($8.73) weekly over a year. Since obtaining the loan, her pet shop’s earnings have doubled, providing financial stability for her household.

Sedeño has been a client of CARD, Inc. since 2007, and her latest and largest loan of ₱100,000 ($1,748) in 2023 helped expand her e-loading and remittance business. The loan, payable at ₱2,560 ($44.70) per week over a year, provides the necessary working capital to handle large outgoing remittances and fund her business operations.

Her business flourished as the only payment center in a village of 1,000 households. With the profits, Sedeño built two houses for her family of six and purchased a car. She also benefited from CARD Inc.’s training programs, such as on bookkeeping.

CARD, Inc.’s philosophy encourages clients to develop alternate income streams, ensuring a safety net in case one’s primary income source is disrupted. This led Sedeño to work at the same time as an online tutor and a real estate agent. “Because of CARD, Inc.’s help, we have obtained financial freedom. Now, we can buy not just our needs but also our wants,” she said.

Through their entrepreneurial efforts and the backing of a supportive lender, these two women have transformed their families’ lives, embodying resilience, financial stability, and empowerment.

Inclusive business strategy

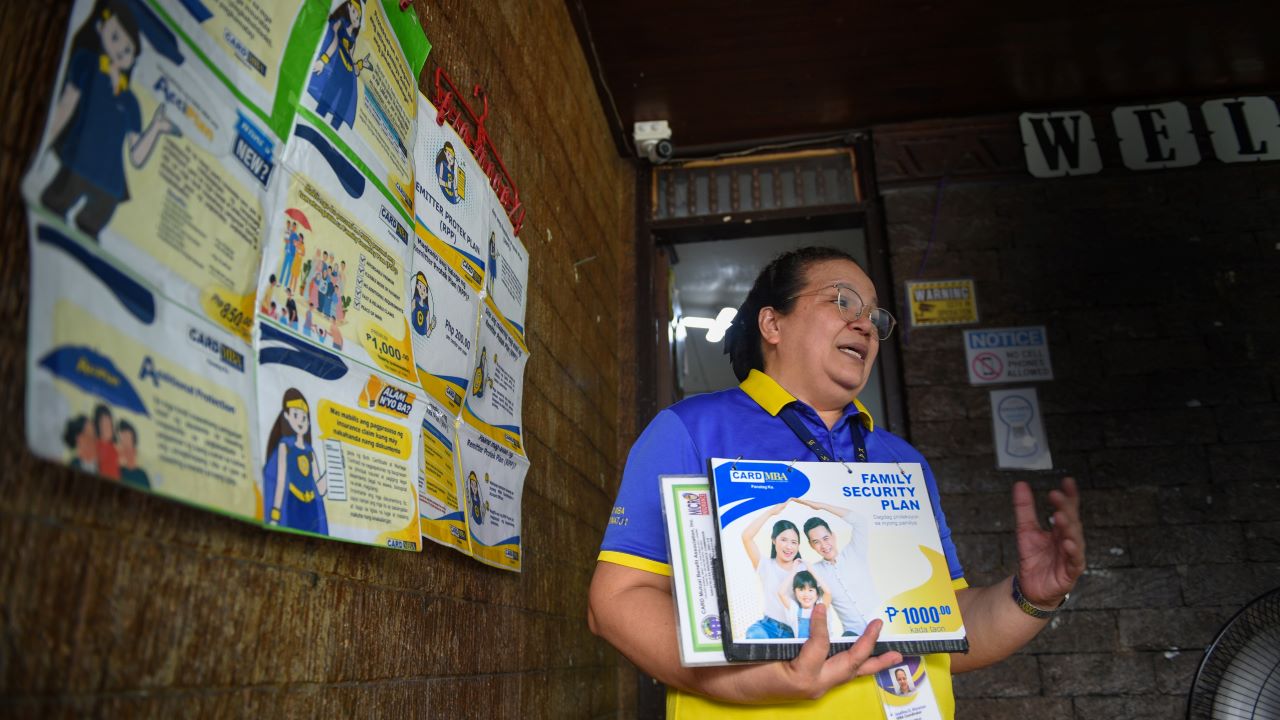

CARD, Inc.’s inclusive business model is designed specifically to cater to the needs of low-income individuals and communities. It uses an approach where borrowers apply individually through small groups, called centers, and borrowers’ family members act as coborrowers who share the obligation to repay the loan. This approach not only helps mitigate the risk of default but also fosters a sense of responsibility among family members, which can improve loan repayment rates.

Unlike traditional banks, CARD, Inc. does not require collateral from its borrowers because its primary mission is to provide financial services to low-income individuals (often in underserved or impoverished areas) who do not have assets or property suitable as collateral. It also helps borrowers build savings and capital by requiring regular deposits, in accordance with government policies for NGOs. Borrowers must deposit at least ₱50 ($0.86) weekly, which the borrowers can withdraw after availing themselves of a loan. CARD, Inc. offers a higher interest rate on these deposits than commercial banks to encourage saving.

CARD, Inc. reaches out to potential clients nationwide. Low-income clients are recruited in two ways. In areas with an existing office, CARD, Inc. relies on referrals from clients. In areas with no existing offices, account officers coordinate with mayors and barangay (village) officials to identify poor families and potential clients. If there are at least 20 potential clients, CARD, Inc. sets up a center in the area.

CARD, Inc. uses the Poverty Probability Index tool to screen potential microfinance clients and measure poverty. “Through this tool, we do not only have the full understanding of the economic status and poverty levels of our potential clients, but we are able to tailor our loan products, repayment schedules, and support services to suit the needs and capabilities of borrowers better,” said CARD, Inc. Executive Director Vicente Briones, Jr.

Unlike other microfinance institutions, CARD, Inc. integrates a comprehensive range of services into its microfinance model, including insurance, credit, savings, education, and health services. This holistic approach supports the financial and nonfinancial needs of its clients, aligning with the NGO’s vision to establish a client-owned bank.

Briones said this vision emphasizes not only access to financial services but also ownership and control, with clients actively participating in decision-making processes. CARD, Inc. prioritizes women who demonstrate the capacity to repay loans and are in good physical health, empowering them through inclusive financial solutions and community involvement.

“CARD, Inc. recognizes that ADB’s commitment to developing people and communities closely aligns with its own mission. This shared vision ensures that the partnership is rooted in common goals of promoting sustainable economic development and improving the lives of marginalized populations,” Briones said.

With ADB funding, CARD, Inc. expanded its microfinance loans as of 31 December 2023 to 382,698 clients in 276 branches across the country, with total loans in 2023 amounting to ₱8.7 billion ($149 million).

Lessons and key takeaways

- Focusing on underserved and low-income individuals enables a deeper understanding of their unique challenges. Tailoring products and services to meet their specific needs is crucial for building trust and building long-term relationships.

- CARD, Inc.’s individual lending approach through small groups (centers), with family members acting as co-borrowers, strengthens borrower accountability and encourages repayment. This method mitigates risk by distributing responsibility across family units.

- Insisting on collateral would not work with low-income individuals who lack productive assets. A hands-on and inclusive approach can replace collateral as risk mitigation while simultaneously empowering borrowers and providing financial access to individuals typically excluded by traditional banking models.

- Requiring and incentivizing borrowers to make small, regular deposits builds financial discipline and encourages savings.

- Using tools like the Poverty Probability Index allows organizations to better understand the economic realities of their clients. This data-driven approach helps tailor loan products, repayment schedules, and support services to the specific needs of each borrower.

Manfred Kiefer

Principal Economist, Private Sector Operations Department, Asian Development BankManfred Kiefer is a principal economist at ADB’s Private Sector Operations Department. He is primarily involved in assessing development results of ADB’s investments. Prior to this role, he worked as energy economist and development results specialist at different international financial institutions. He holds an MSc in Economics from Freie Universität Berlin.

Arvin Yana

Consultant, Asian Development BankArvin Yana is an Australia-educated communications specialist with over 2 decades of experience in strategic communication and knowledge management promoting various development programs across different sectors. He has developed a range of communication and knowledge products highlighting ADB's development impact and its significant role in driving progress and transforming lives.

Christian Abeleda

Associate Economics Officer, Private Sector Operations Department, Asian Development BankChristian Abeleda works as an associate economics officer at ADB’s Private Sector Operations Department. He supports private sector projects, particularly in the agribusiness sector, by preparing economic evaluations and enhancing development impacts perspectives. His research focus is on monitoring and evaluation of impacts of agricultural development projects.